News

What changes are happening to R&D Tax Relief from April?

21 Feb 2023

Following his appointment as Chancellor, Jeremy Hunt announced major changes to the Research and Development (“R&D”) scheme, which will see some winners but many more losers as the rates of relief are set to be cut dramatically from April 2023 and with further changes also due soon after.

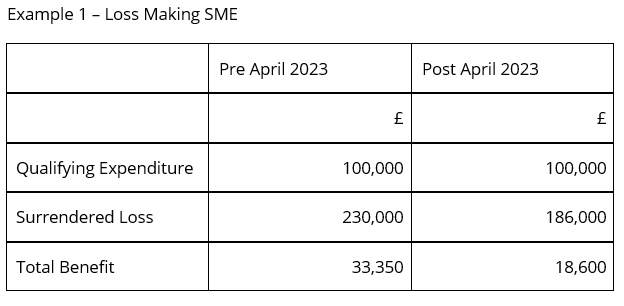

Currently, the tax relief for SMEs is extremely generous as it allows for a tax deduction which exceeds the original amounts spent or, in a lot of instances, creates a cash payment for losses surrendered.

The enhanced rate for R&D expenditure for SME’s is 130%; however, the planned change will see this reduced to 86%, with the payable credit being reduced from 14.5% to just 10%. Loss making SME’s will also see a reduction in the payable credit they receive from 33% credit on qualifying expenditure to just 19%.

Author: Charlie Thompson

Senior Tax Consultant

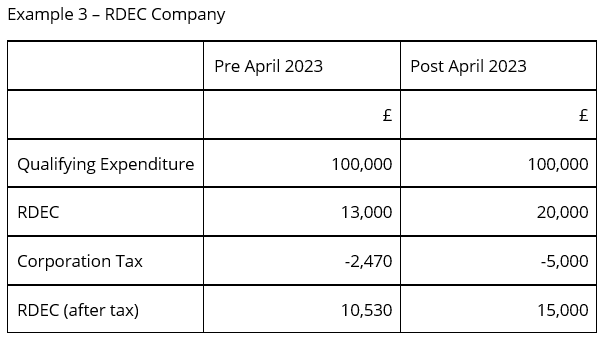

There is good news for companies which apply for the Research and Development Expenditure Credit (“RDEC”). These companies will see an increase in the percentage of payable credit to 20%, currently 13%.

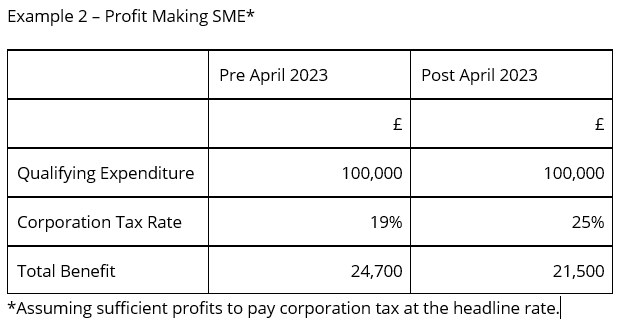

Initially, the above mentioned changes to the level of RDEC payable credit would appear to be a major benefit for those who can claim this; however, when this is looked at with the change to the Corporation Tax Rate increase also planned for April 2023 (from 19% to 25%), and upcoming changes to relief for overseas R&D, the above rate increase would more simply appear to be mitigating other tax increases.

In addition, further changes include:

1. Claims must be made digitally. Currently there is an option for some changes to be made by post. This will likely make it easier for HMRC to review the claim.

2. Claims must include specific information, such as the breakdown of specific types of expenditure.

3. A named officer of the company must approve claims. This should help prevent unscrupulous claims made by third parties without keeping the company informed.

4. Claims must include details of any associated agents.

5. Companies must submit a pre-notification of their claim within 6 months of the period end, unless they have claimed in the last three years. This will limit the benefit of R&D for new companies, as they will not be able to claim for a previous period which they can currently.

At WR Partners, all R&D claims are included on a detailed report, showing breakdowns of qualifying expenditures, and details of the qualifying projects, stating the client approves our firm name and the report.

If you would like assistance in claiming R&D tax relief, don’t hesitate to contact us.

Visit our dedicated R&D hub

We love meeting new, exciting businesses. Get in touch with our team to see how we could enhance and protect your financial position.

Or if you’d prefer to speak to someone directly just give us a call on: 08000 664 664 or email: hello@wrpartners.co.uk.

"*" indicates required fields